Wednesday, August 29, 2007

| [+/-] |

Doctorate to Director Shankar, Hero Vijay |

Labels:

Entertainment News

| [+/-] |

Emkay Deal Update : JSW Steel Buys US arm of Jindal Saw via LBO route |

(BSE: 500228 | NSE: JSWSTEEL | ISIN: INE019A01020)

JSW has acquired 90% stake in the US arm of Jindal Saw (JSAW). JSAW has a plate mill capacity of 1.2mtpa, Lsaw pipe capacity of 0.55mtpa and W-jointing capacity of 0.35mtpa. JSW has valued the US operations of JSAW at an EV of USD900mn. The existing shareholders will retain 10% stake, while JSW will acquire balance 90% stake through the LBO route with a cost of debt at LIBOR + 2.5%. The US operations posted EBITDA of USD75mn for the period July 2006-June 2007. However, the company has calculated proforma EBITDA of USD143.9mn after various notional adjustments to

arrive an EV/EBITDA of 6.25x for the acquisition. Although we believe the deal is expensive as compared to the cost of acquiring the assets, but the premium can be attributed to the fact that JSW has not only acquired the assets of the company, but also the facilities which are accredited by the customers that will take a long time to replicate. JSW currently has one million tonne excess slab, which it plans to ship to US thereby reducing the cost of production at its plate mill facility substantially. JSW has stated that the deal will be EPS accretive at the consolidated level in the first year of operations itself. We are positive on the deal. We will revise our earnings estimate post evaluation of the earnings accretion from the deal. We continue to maintain a buy on the stock with a target price of Rs790, which is 7x FY09 earnings prior to the deal.

The deal structure JSW will acquire 90% stake in the combined US operations of Jindal Saw. The entire funding for the deal will be through debt raised at various levels of holding.

Rationale for the acquisition JSW currently has a slab capacity of 3.8mtpa and rolling capacity of 2.8mtpa. The company intends to ship the surplus 1mtpa slab it currently has to the US operations and add value there to increase the realization. Currently the company is selling slabs at USD500-525/t. The pipes are likely to fetch around USD1,500-1,600/t in the current market scenario.

Why the US operations under JSAW not been satisfactory? The US operations of JSAW was primarily based on tolling agreement where the Jindal United Steel Corporation and Saw Pipes USA worked mainly on a tolling agreement leading to lower margins. Secondly, as per the management, the JSAW management have not incurred the maintenance capex which has lead to a significant increase in down time, thereby reducing the productivity of the mills. Lastly, but most importantly, the US operations have been badly hurt by irregular and poor quality slabs being supplied for rolling and finishing which increased the yield loss to 19% and scrap generation to the tune of 14%.

How does JSW plan to increase efficiency and reduce costs at JSAW JSW plans to ship slabs from the Vijaynagar facility sized as per exact requirement at the US facilities thereby eliminating the need for 31 employees who are currently utilized only for sizing the slabs. This action will itself reduce the yield loss from 19% to ~13% and also reduce scrap generation. Further, the company is planning to increase the production of saw pipes from 200,000t in FY07 to 350,000t in FY08 and further increase it to 500,000t in FY09. Similarly, JSW also plans to increase the plate mill production from 600,000t in FY07 to 850,000 in FY08 and further to 1,000,000t in FY09. JSW is also likely to incur additional capex of USD61mn for repairs and modernization of the mill which will further help reduce the downtime and thereby increasing productivity of the mill. Out of the total payout of USD810mn (excluding inventory value), we estimate the share of Mr. P.R. Jindal will be around USD466mn. In addition, Jindal SAW will continue to hold 10% in the new SPV, JSW US-Holding-SPV-2.

Valuations Although we believe the valuation of the target companies especially the Saw Mill appear to be stretched, the acquisition does make a business sense. JSW with its excess slab capacity will have the opportunity to tap into the lucrative oil and gas pipes market in US. Further the company will incur a capex of USD61mn for repairs and modernization of the pipe making facility, which will then utilize the in-house plate mill capacity to the fullest. We believe the deal is likely to be EPS accretive to JSW on a consolidated basis as there is no equity dilution and additional interest burden for funding will be close to USD80mn. The target companies had actual combined EBITDA of USD75mn in Jul-Jun2007 due to external slab supplies and other negative factors. We believe the EBITDA in financial year can improve significantly. We continue to remain positive on the long-term prospects of the company and its valuation at the current levels, excluding the deal. We continue to maintain a buy on the stock with a target price of Rs790, which is 7x FY09 earnings prior to the deal.

Key Risks Due to the current acquisition, the debt-equity of the company is likely to breach its target of 1x in the short run. The company expects the debt-equity to shoot to 1.4-1.5x in the current year. However, the ratio is expected to moderate as soon as the US operations are stabilized.

Other Info: Corporate Announcements | Board Meetings | Financial Results | Corporate Actions

Company Address | Shareholding Pattern | Results Comparison

To Download Full Research Report

Investment in equity shares has its own risks. Sincere efforts have been made to present the right investment perspective.The information contained herein is based on analysis and up on sources that we consider reliable. I, however, do not vouch for the accuracy or the completeness thereof. This material is for personal information and I am not responsible for any loss incurred based upon it.& take no responsibility whatsoever for any financial profits or loss which may arise from the recommendations given in this blog.

Labels:

Finance

| [+/-] |

Anandrathi : Market Outlook (Medium Term View) |

The sensex ended negative in what can be termed as one of the most volatile day in trading history. Market participants are clearly nervous due to the current uncertainty about the impact of the damage to banks and hedge funds from the sub prime mortgage crisis internationally. Add to this the delicate political situation, possibility of early elections have only added to the nervousness.

In the press conference post market, Left announced that it did not intend to destabilize the Government but is against the deal and will take appropriate action if Congress goes ahead with the nuclear deal. Meanwhile they intend to continue protesting the deal.

Sensex lost 0.59 percent while mid cap index lost 0.88 percent. The small cap index lost more than a percent. Among sectoral indices, fmcg managed to end the day in positive ending up more than a percent. We have seen buying interest here in stocks like ITC, Hind Lever. Any sharp dips can be used by value buyers to get into these stocks. Banking sector lost ground and ended the day 2.2 percent down. Frontline banking stocks like ICICI, SBI, PNB lost ground here while the mid-cap PSU banks were holding ground. Some stability is returning into the technology sector which also managed to hold on.

For all the talk about political crisis and given the extent of volatility, the FII and DII data does come as a surprise. Both were net buyers in the cash market. FIIs bought Rs 274 cr. while DIIs were net buyers of Rs 530 cr in cash market as per provisional data. Even in the futures segment, FIIs were net buyers of about Rs 1100 cr.

After a long period, we have seen FIIs turning net buyers in the cash market and this despite the fluid political situation. The international markets have held ground despite concerns continuing over the impact of sub prime crisis on the economy going ahead. BOJ held on to the rates for the time being given the current turmoil in financial markets. Market participants seem to have over reacted and panicked about the Left Press Conference and since nothing really came out of the same, we can expect markets to pull back. Telecom, capital goods, cement, auto are some of the areas which could see smart upmove in a pull back.

Corporate News:

Everest Industries Ltd (EIL) , has set a target of 20 per cent growth in sales this fiscal and is eyeing Rs 500 crore turnover by FY 2008-09. The company is setting up a manufacturing unit at Roorkee in Uttarakhand at an investment of Rs 75 crore and it will be commissioned this fiscal. The company is setting up a manufacturing facility at Roorkee in Uttarakhand at an investment of Rs 75 crore. The facility is nearly complete and is expected to start the commercial operation by the end of the present fiscal. The manufacturing capacity of Roorkee plant will be 122,000 metric tonnes of roofing sheets and 60,000 metric tonnes of flat boards per year and 600 solid wall panels per day.

Bajaj Electricals is looking to acquire premium brands in appliances in its pursuit of growth. The company plans to double its turnover in two years and quadruple it in six years, through acquisitions in its existing businesses and foraying into new areas that may include tie-ups with international players. The company would raise its turnover from the current Rs 1,100 crore to Rs 2,100 crore by 2009-10 and to Rs 4,000 crore by 2012-13. The journey to this Goal will be on the back of expanded market share in the existing lines of business as well as new product lines, including products sourced from international majors. The company has already tied up with Italian appliances major, Nardi, to market its gas-based cooking appliances in India . The range includes gas stoves and chimneys and this would be extended to premium and ultra premium offerings. These products may not form a major part of our business in terms of the number of units, but will add significantly to the top line.

Bharat Heavy Electricals Limited (BHEL ) is set to ramp up the capacity of its boiler auxiliaries plant (BAP) at Ranipet to 10,000 Mw in the next two years. The move is part of the corporate plan to scale up the overall capacity to 15,000 Mw, which includes contributions towards hydro power and nuclear power besides the thermal power sector. For the current year, the order book position is at Rs 1,457 crore as against Rs 1,266 crore in the previous year. The eastern region alone accounts for about 18 per cent of the total sales volume of Tata Motors and they are targeting to raise this share.’Ace’ clocked a sales volume of over 5000 in the state last year and is expected to cross the 8000 mark in 2007- 08,

Standard Chartered has entered into an agreement to acquire 49% stake in UTI Securities from the Securities Trading Corporation of India (STCI) with an option of increasing its stake to 100% over the next three years. It has picked up the 49% stake at Rs 147 crore, valuing UTI Securities at Rs 300 crore. STCI had in February 2006 bought UTI Securities from the Specified Undertaking of the Unit Trust of India (SUUTI) for Rs 265 crore. They have an option to purchase the balance at a pre-determined formula in 2010. The move will help give our customers a wider product portfolio.

To Download The full Report

completeness. Neither the information nor any opinion expressed constitutes an offer, or an invitation to make an offer, to buy or sell any securities, options, future or other derivatives related to such securities (“related investment”). ARS and its affiliated may trade for their own accounts as market maker/ jobber and /or arbitrageur in any securities of this issuer(s) or in related investments, and may be on the opposite side of public orders. ARS, its affiliates, directors, officers, and employees may have a long or short position in any securities of this issuer(s) or in related investment banking or other business from, any entity mentioned in this report. This research report is prepared for private circulation. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. Investors should seek financial situation and the particular needs of any specific investing in any securities or investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. Investors should note that income from such securities, if any, may fluctuate and that each security’s price or value may rise or fall. Past performance is not necessarily a guide to future performance. Foreign currency rates of exchange may adversely affect the value, price or income of any security or related investment mentioned in this report.

Investment in equity shares has its own risks. Sincere efforts have been made to present the right investment perspective.The information contained herein is based on analysis and up on sources that we consider reliable. I, however, do not vouch for the accuracy or the completeness thereof. This material is for personal information and I am not responsible for any loss incurred based upon it.& take no responsibility whatsoever for any financial profits or loss which may arise from the recommendations given in this blog.

Labels:

Finance

Tuesday, August 28, 2007

| [+/-] |

ICICI Direct : Buy Man Industries (India) (MANIN) |

(BSE: 513269 | NSE: MANINDS | ISIN: INE993A01018)

Company Background Man Industries (India) Ltd, the flagship company of the Man Group, UK, manufactures steel line pipes for high and medium pressure applications such as oil and gas, petrochemical and water transportation, anti-corrosion coating systems and aluminum extrusion products. The company started operations in 1989 as an aluminium extrusion company with an installed capacity of 4,000 tonne per annum (tpa). In 1994, it set up a Submerged Arc Welded (SAW) pipe plant in Pithampur, Madhya Pradesh. In 1998, it became an integrated SAW pipe manufacturer with its own polyethylene-coating facility as part of its forward integration plan. It also set up a spiral pipe-making mill. In FY05, the company expanded capacity by setting up another plant in Anjar, Gujarat. Post expansion, the combined capacity increased to 2,000 km of pipes per annum.

Investment Rationale Robust global demand boom Demand for SAW pipes is likely to remain firm in next five years due to burgeoning crude prices and depleting oil reserves. We expect global demand to be in the range of 67 million tonnes with around 66% flowing in from Middle East, Asia & US, the key markets for the Indian players. While demand in Europe and Russia would be met by internal supplies, demand in Middle East and US is likely to be met through imports. This high demand, coupled with supply constraints, would keep prices firm at for least two years through CY08 and 09, escalating to mid 2010, where after it may start softening.

Diversification the key attraction Man Industries’ business would be split equally between LSAW and HSAW pipes from December 2007. HSAW pipes are manufactured from hot-rolled (HR) coils, which is easily available at comparatively lower price. In contrast, LSAW are manufactured from plates, which are in short supply. Though the two types of pipes are interchangeable, the high price of LSAW pipes may put pressure on demand. The diversification would de-risk its business. Despite their high price, we believe LSAW pipes would continue to score better than the HSAW in terms of profitability as manufacturing cost of LSAW is around 50% that of HSAW. Further, the scrap generated from LSAW is also minimal. The yield in HSAW is 90-96% while that in LSAW is as high as 99.5 100%. Currently, the difference in prices for plates (raw material for LSAW) and hot rolled coils (raw material for HSAW) is between US$250-300 per tonne for different grades of steel. A lot of units to manufacture plates are being set up and we expect prices to decline in the next few years. We expect prices of plates to fall and the price differential between plates and coils will decline to US$0-100. We believe lower raw material prices would result in LSAW prices decline.

Timely capex, robust order book gives earning visibility Man Industries is in capex mode and post expansion, its capacity of 1 million tonnes would be more than 2x the existing capacity, equally distributed between LSAW and HSAW pipes. This would reduce the risk and increase the size of addressable market. With a robust order book position of Rs 2,400 crore, we expect the top line to grow at a CAGR of 51% over FY07-09E and net profit by 67%. Capacity utilization should be at about at 40% in FY09E.

Risk and Concerns Man Industries exports its products mainly to companies in the Middle East. About 90% of the current orders are from abroad. Any appreciation in the rupee could impact the company’s financial performance. Freight cost is an important cost for pipe manufacturers. A rise in freight charges could the bottom line. Capacity expansion by other players around the world or by new entrant may put pressure on realizations. A large number of players could result in the bargaining power of buyers increasing and manufacturers would not be able to pass on rises in raw material costs to buyer.

Financials In FY07, the company reported a top line of Rs 1,133.10 crore and a bottom line of Rs 55.30. In the Q108, sales grew 54% y-o-y to Rs 320.99 crore while bottom line grew 67% y-o-y to Rs 17.35 crore. The plant at Anjar started operations whereby the company increased the execution of new orders. Moreover, the company also witnessed traction in capacity utilization to around 45% on the current capacity of 600,000 tpa. From Q408, we expect the company would operate at the total capacity of 1 million tonnes. We expect the robust order book to drive the company’s top line at a CAGR of over 51% during FY07-09E to Rs 2,116.25 crore and bottom line at a CAGR of around 67% to Rs 153.71 crore.

Valuations Man Industries is set to capitalize on the rising global demand for pipelines. At the current price of Rs 255, the stock is trading at 4.42x the FY09E EPS. We expect orders from oil & gas clients to drive the growth momentum going forward and expect the stock to touch Rs 306, an upside of 20%, within a 3-6 month timeframe.

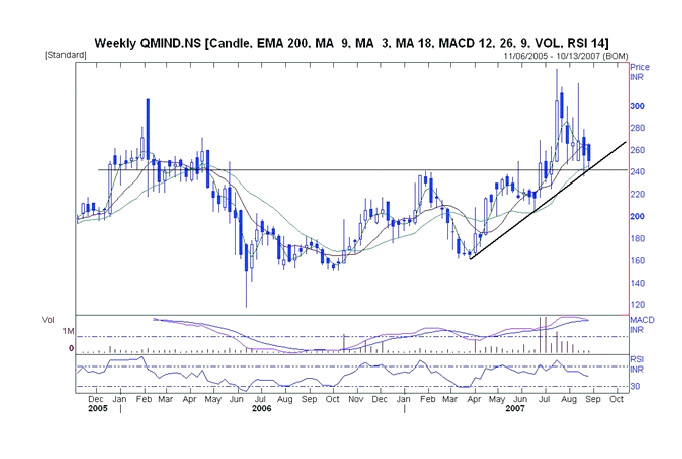

Technical Outlook The stock has broken above a long-term resistance at Rs 240. It had thereafter hit a high of Rs 320. It has now begun consolidating and is finding support at Rs 240. It has also formed a bullish rounding bottom formation. Momentum indicators remain in overbought zones. They are expected to come down after the consolidation before the next bullish impulse begins.

Other Info: Corporate Announcements | Board Meetings | Financial Results | Corporate Actions

Company Address | Shareholding Pattern | Results Comparison

Every week, the ICICIdirect research team selects a stock based on fundamental and/or technical parameters, which is likely to give a return of 20% or more over a 3-6 month perspective.

Investment in equity shares has its own risks. Sincere efforts have been made to present the right investment perspective.The information contained herein is based on analysis and up on sources that we consider reliable. I, however, do not vouch for the accuracy or the completeness thereof. This material is for personal information and I am not responsible for any loss incurred based upon it.& take no responsibility whatsoever for any financial profits or loss which may arise from the recommendations given in this blog.

Labels:

Finance

Subscribe to:

Posts (Atom)